Presented by Mark Gallagher

General market news

• The yield on the 10-year Treasury was back down to its recent low of 2.79 percent late last week after reaching as high as 2.95 percent. It opened at 2.83 percent early Monday. The 30-year was as low as 3.07 percent last week before opening at 3.11 percent Monday morning. The 2-year was back down to 2.21 percent Monday after being as high as 2.28 percent late last week.

• Each of the three major U.S. indices, as well as the Russell 2000 Index, lost at least 1 percent last week. During the week, the market digested news of Jerome Powell’s first testimony before Congress. The newly appointed chair of the Federal Reserve was candid in his comments on the economy, which he believes to be strong. His testimony seems to have led investors to believe that he may be more hawkish in raising rates.

• Other major news affecting the markets was President Trump’s proposed 25-percent tariff on steel and 10-percent tariff on aluminum. The move has many questioning what is ahead for NAFTA and other trade agreements.

• The economic data released last week was a mixed bag; the hard figures were weak, while the soft business and consumer confidence measures were strong. On Monday, new home sales declined sharply, against expectations for a modest increase.

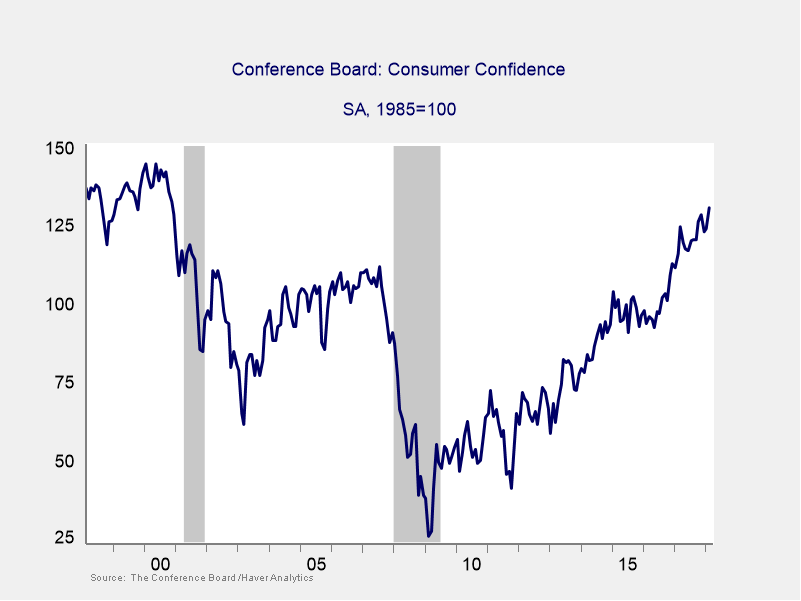

• On Tuesday, durable goods orders declined at both the headline and core level. Also on Tuesday, the Conference Board Consumer Confidence Index surged to a 17-year high, despite volatility in the equity market.

• On Wednesday, the second estimate of fourth-quarter gross domestic product declined, as expected, to 2.5-percent growth, down from the initial estimate of 2.6 percent. Even with this minor downward revision, the economy was healthy in 2017, growing at 2.3 percent on a real basis.

• On Thursday, the personal income and spending reports were both largely in line with expectations. Also on Thursday, the Institute for Supply Management’s (ISM) Manufacturing index rose to a 13-year high, which should help spur additional growth in manufacturing to begin the year.

| Equity Index | Week-to-Date | Month-to-Date | Year-to-Date | 12-Month |

| S&P 500 | –1.98% | –0.81% | 1.01% | 15.23% |

| Nasdaq Composite | –1.05% | –0.19% | 5.33% | 25.16% |

| DJIA | –2.97% | –1.96% | –0.30% | 19.59% |

| MSCI EAFE | –2.86% | –2.24% | –1.95% | 17.53% |

| MSCI Emerging Markets | –2.80% | –1.09% | 2.23% | 29.50% |

| Russell 2000 | –1.00% | 1.39% | 0.01% | 11.31% |

Source: Bloomberg

| Fixed Income Index | Month-to-Date | Year-to-Date | 12-Month |

| U.S. Broad Market | –0.02% | –2.11% | 1.16% |

| U.S. Treasury | 0.08% | –2.03% | 0.25% |

| U.S. Mortgages | 0.05% | –1.77% | 0.84% |

| Municipal Bond | 0.07% | –1.41% | 3.16% |

Source: Morningstar Direct

What to look forward to

We’ll see three major economic reports this week, which will give us a look at the service sector, trade, and the job market.

On Monday, the ISM Nonmanufacturing index was released. It did better than expected, dropping slightly from 59.9 in January to 59.5 for February, against expectations for a drop to 59. Although this index has been volatile in recent months, the trend has remained positive. Because this is a diffusion index, values above 50 indicate expansion, so even with the decline, the index still indicates strong growth. With the ISM Manufacturing index’s good results last week, this result shows business confidence remains strong across the board.

On Wednesday, the international trade report is expected to show that the trade deficit improved slightly, from $53.1 billion in December to $52.6 billion in January, on a rise in exports due to the weak dollar and strong global growth. There is some downside risk here, but if the numbers come in as expected, trade could be less of a drag than expected on economic growth in the first quarter of 2018.

Finally, on Friday, the employment report is expected to show continued job growth, with 200,000 jobs added in February, the same as in January. Wage growth is also expected to stay constant at a healthy 0.3 percent. Meanwhile, labor demand, as expressed by the average workweek, is expected to rise from 34.3 hours to 34.4 hours. There may be some upside risk here, as jobless claims have continued to drop and employment surveys have remained strong. Overall, if the report is as expected, it will be another positive signal for continued growth.

There’s one more piece of economic news to watch for: whether the White House follows through on the steel and aluminum tariffs President Trump announced last week. Markets around the world pulled back on the news, and any follow-through could result in more volatility.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg Barclays US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg Barclays US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg Barclays US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million.

Mark Gallagher is a financial advisor located at Gallagher Financial Services at 2586 East 7th Ave. Suite #304, North Saint Paul, MN 55109. He offers securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. He can be reached at 651-774-8759 or at mark@markgallagher.com.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2018 Commonwealth Financial Network®