Presented by Mark Gallagher

General Market News

• Rates continued to fall last week, as concerns about the spread of the coronavirus rattled global markets. The 10-year Treasury yield opened at 1.38 percent, nearing lows last seen in 2016. The 30-year fell to 1.83 percent, which is its all-time low.

• Markets were down across the globe last week. Investors took a risk-off approach due to concerns about the spread of the coronavirus to areas beyond China. The increase in cases in countries such as South Korea, Iran, and Italy led to fears that what was once an epidemic more or less contained within China may become a global pandemic. The removal of passengers from the Japanese cruise ship Diamond Princess added to the number of cases outside of China.

• Not surprisingly, the bond proxies in REITs, consumer staples, and utilities were among the top-performing sectors on the week. Investors moved away from technology, financials, and consumer services, which were the worst-performing sectors.

• The National Association of Home Builders Housing Market Index for February was released on Tuesday. This measure of home builder confidence slid modestly from 75 in January to 74 in February, against expectations to remain flat for the month. The index remains just two points off of the 20-year high of 76 that was set in December. Geographically, results were mixed, with confidence in the South and the Northeast reaching new highs, while sentiment in the West and Midwest decreased slightly.

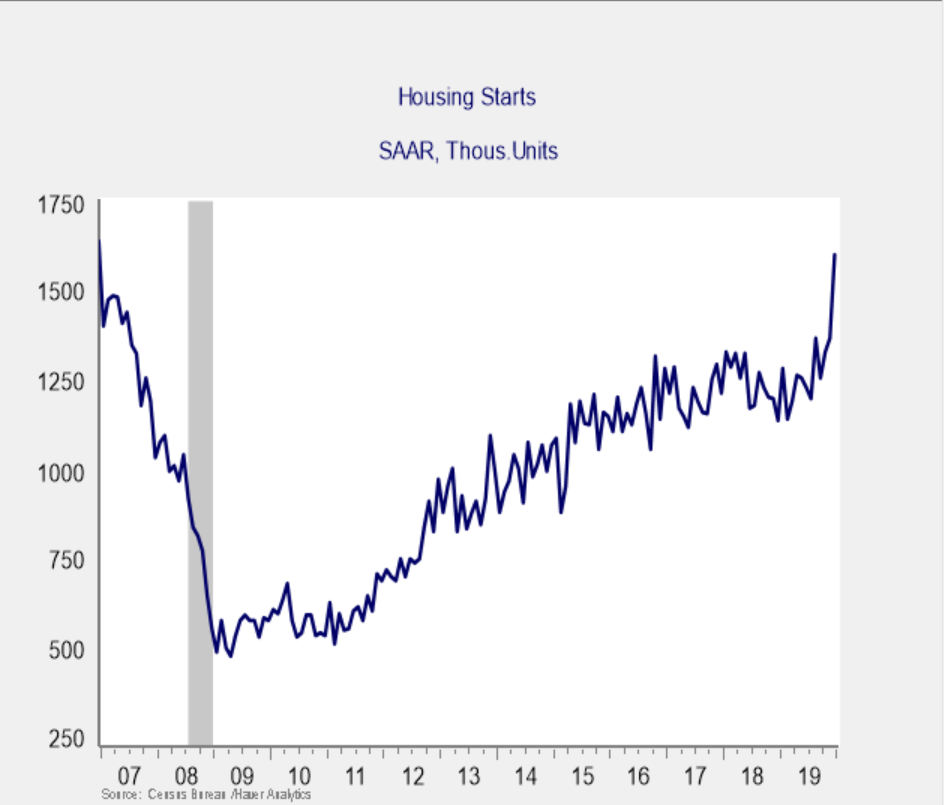

• We didn’t have to wait long to see the positive effects of high home builder confidence at the start of the year, as January’s building permits and housing starts reports came in better than expected. Permits increased by 9.2 percent during the month, against expectations for a 2.1 percent increase. Starts declined by 3.6 percent, but this was far better than economist expectations for an 11.2 percent decline. These two data points can be volatile on a month-to-month basis; however, both permits and starts showed a clear upward trend in the second half of 2019 that has continued into the new year. Permits now sit at their highest monthly level since 2007, while starts are at their second-highest monthly level over the same time period. So, the monthly volatility is nothing to worry about.

• Wednesday saw the release of January’s Producer Price Index report. Producer inflation increased by 0.5 percent during the month against expectations for a 0.1 percent increase. This brought year-over-year producer inflation up to 2.1 percent, which is much higher than December’s year-over-year inflation rate of 1.3 percent. Core producer inflation, which strips out the impact of volatile food and energy prices, showed similar monthly growth of 0.5 percent and year-over-year growth of 1.7 percent. Most of the increase can be attributed to higher costs for services, which make up roughly 65 percent of the headline figure and rose by 0.7 percent during the month. Despite the faster-than-expected growth for the month, on a year-over-year basis, inflation remains below recent highs set in 2018 and 2019. The Federal Reserve (Fed) has indicated it is willing to let inflation run above its state 2 percent target for the time being.

• Speaking of the Fed, the minutes from the January Federal Open Market Committee meeting were released on Wednesday. The Fed voted unanimously to keep the federal funds rate unchanged, and there were few major revelations from the minutes. Overall, Fed members appeared to be a bit more optimistic about the economic expansion; however, there was some discussion about the spread of the coronavirus from China and the potential effects that could have on global growth. They also discussed the plan to wind down their involvement in the repurchase market, which they anticipate will likely happen in the second quarter. Overall, the impact of this release was relatively minimal, as it echoed much of what Fed Chair Powell stated to Congress when he presented the semiannual Monetary Policy Report earlier in the month.

• We finished the week with Friday’s release of January’s existing home sales report. Sales declined by 1.3 percent during the month, but this was better than the expected 1.8 percent decline. On a year-over-year basis, sales are up more than 10 percent. This marks seven straight months with year-over-year growth for existing home sales, which is a strong turnaround following the prolonged slowdown in sales throughout 2018 and at the start of 2019. Housing’s rebound has been one of the bright spots of the economic expansion over the past few quarters, and this result indicates prospective home buyers are still willing and able to continue to fuel the expansion.

| Equity Index | Week-to-Date | Month-to-Date | Year-to-Date | 12-Month |

| S&P 500 | –1.22% | 3.63% | 3.59% | 21.89% |

| Nasdaq Composite | –1.55% | 4.75% | 6.88% | 28.58% |

| DJIA | –1.36% | 2.85% | 1.94% | 14.06% |

| MSCI EAFE | –1.24% | 0.57% | –1.53% | 10.28% |

| MSCI Emerging Markets | –1.96% | 2.11% | –2.65% | 5.02% |

| Russell 2000 | –0.52% | 4.08% | 0.74% | 7.10% |

Source: Bloomberg

| Fixed Income Index | Month-to-Date | Year-to-Date | 12-Month |

| U.S. Broad Market | 0.57% | 2.47% | 10.07% |

| U.S. Treasury | 0.77% | 2.93% | 9.45% |

| U.S. Mortgages | 0.21% | 1.05% | 6.51% |

| Municipal Bond | 0.55% | 2.35% | 8.74% |

Source: Morningstar Direct

What to Look Forward To

On Tuesday, the Conference Board Consumer Confidence Index for February will be released. Economists are forecasting a modest increase, from 131.6 in January to 132.1 in February. This result would match the month’s gains in the University of Michigan consumer sentiment survey. Consumer confidence hit a five-month high in January, after remaining rangebound for the fourth quarter. Higher confidence levels support additional spending growth, so an increase would certainly be regarded as a tailwind for future growth.

On Wednesday, January’s new home sales report is scheduled for release. Sales are expected to increase by 2.3 percent during the month, up from a modest 0.4 percent decrease in December. Compared with existing home sales, new home sales are a smaller and more volatile portion of the housing market. Still, they showed a notable uptick in the second half of 2019. If the January estimate proves accurate, it would represent the fastest pace of new home sales since 2007, providing another example of the housing sector’s strength.

On Thursday, we’ll get the second estimate of fourth-quarter gross domestic product growth. Economists believe the annualized pace of economic growth in the fourth quarter will be revised up from 2.1 percent to 2.2 percent. Personal consumption is expected to remain flat at a 1.8 percent annualized growth rate. If the estimates hold, they would mark an acceleration from the 2.1 percent growth rate achieved in the third quarter. Economists had previously forecasted 2 percent growth for the fourth quarter, so any additional improvements from the early estimate would certainly be positive.

Thursday will also see the release of the preliminary durable goods orders report for January. Orders are set to decline by 1.5 percent, following a better-than-expected 2.4 percent increase in December. Headline durable goods orders experienced a high level of monthly volatility during the fourth quarter, primarily driven by swings in defensive aircraft orders. Core durable goods orders, which strip out the effect of volatile transportation orders, are set to increase by 0.2 percent, up from a 0.1 percent decline in December. Core durable goods orders are often used as a proxy for business investment, so this anticipated increase would be quite welcome, especially given the decrease in core orders in November and December. Previously released surveys showed business confidence picking up in January, so there’s reason to believe that investment will also increase. This would be a good sign for overall growth, given the lack of business investment throughout much of 2019.

On Friday, January’s personal income and personal spending reports will be released. Both are expected to show 0.3 percent monthly growth. These results would be a solid start to the year for consumers, who were the major drivers of the economic expansion in 2019. Income and spending grew at similar rates throughout 2019, indicating that spending growth will be sustainable. As long as consumers are earning more and willing to spend more, the prospects for continued growth remain strong.

Finally, we’ll finish the week with the second and final reading of the University of Michigan consumer sentiment survey for February. Economists expect to see a slight pullback for the index from the midmonth reading of 100.9 to 100.6 at month-end. The first midmonth estimate came in above economist forecasts of 99.5, so this anticipated decline would still leave the survey above initial estimates for the month. Consumer sentiment has so far remained impressively resilient despite the continued spread of the coronavirus from China. It will be important to keep monitoring this sector, however, given the relationship between rising confidence and spending growth.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg Barclays US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg Barclays US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg Barclays US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million.

Mark Gallagher is a financial advisor located at Gallagher Financial Services at 2586 East 7th Ave. Suite #304, North Saint Paul, MN 55109. He offers securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. He can be reached at 651-774-8759 or at mark@markgallagher.com.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2020 Commonwealth Financial Network ®