Presented by Mark Gallagher

General market news

• The yield on the 10-year Treasury opened at 2.33 percent on May 15, after being as high as 2.42 percent the prior week. The yield fell in reaction to news that the U.S. Consumer Price Index rose 0.2 percent in April, a sign that inflation may be stabilizing. The 30-year yield also moved lower, settling around 3 percent.

• Markets were mixed last week. The S&P 500 snapped its streak of consecutive weekly gains at four, falling 0.26 percent. The Dow Jones Industrial Average also pulled back a modest 0.35 percent. The Nasdaq Composite fared better, rising 0.42 percent on strong earnings from Nvidia and news that Apple had surpassed $800 billion in market capitalization—the first company to do so.

• Despite many changes in the geopolitical environment over the past week, the markets seem complacent, as the CBOE Volatility Index (VIX) closed at its lowest level since 1993. The election of Moon Jae-in as president of South Korea and Emmanuel Macron as president of France yielded little reaction. Likewise, markets were unmoved by the surprise firing of FBI Director James Comey. Still, the decision has many questioning whether it will create additional headwinds for the new administration and its desired changes to health care and tax policies.

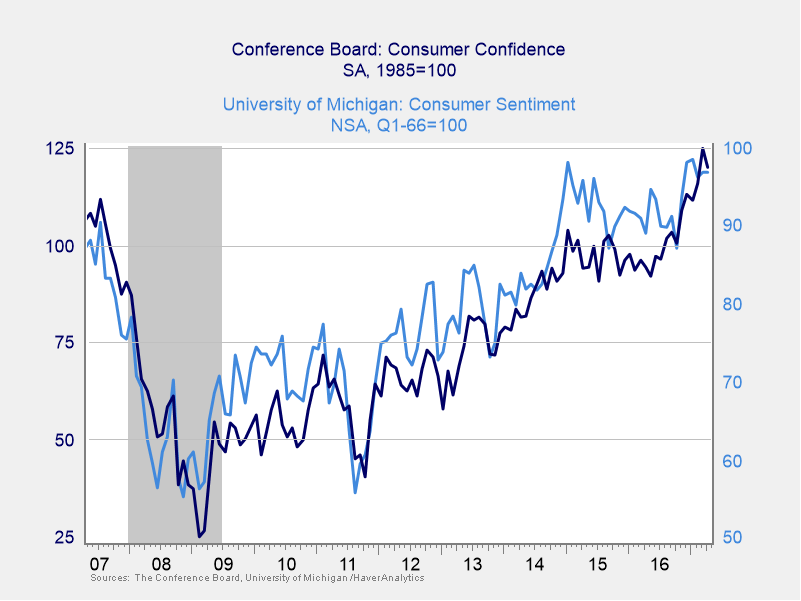

• Last week’s economic data, which focused primarily on consumers, was moderately positive. Retail sales data came in slightly below expectations, with month-over-month growth of 0.4 percent. Much of the increase was attributed to a healthy 0.7-percent uptick in auto sales. The University of Michigan Consumer Sentiment data surprised observers by moving higher despite expectations for no change. Consumer sentiment remains near highs last seen in the early 2000s. Combined with the rebound in auto sales and the elimination of weather-related headwinds, this data has analysts expecting significantly higher consumption growth in the second quarter.

| Equity Index | Week-to-Date | Month-to-Date | Year-to-Date | 12-Month |

| S&P 500 | –0.26% | 0.40% | 7.58% | 18.30% |

| Nasdaq Composite | 0.39% | 1.33% | 14.17% | 30.76% |

| DJIA | –0.35% | –0.02% | 6.69% | 20.98% |

| MSCI EAFE | 0.35% | 2.17% | 12.64% | 17.18% |

| MSCI Emerging Markets | 2.49% | 2.57% | 16.88% | 27.65% |

| Russell 2000 | –0.98% | –1.20% | 2.34% | 26.52% |

Source: Bloomberg

| Fixed Income Index | Month-to-Date | Year-to-Date | 12-Month |

| U.S. Broad Market | –0.03% | 1.56% | 0.35% |

| U.S. Treasury | –0.17% | 1.20% | –1.41% |

| U.S. Mortgages | –0.05% | 1.08% | 0.33% |

| Municipal Bond | 0.37% | 2.69% | –0.04% |

Source: Morningstar Direct

What to look forward to

The housing market and industrial sector will dominate economic headlines this week.

On Monday, the National Association of Home Builders will release its Housing Market Index. This survey conveys homebuilders’ opinions on the health of the housing industry. It is expected to remain strong and steady at 68, which is close to the 12-year high it reached in March. Downside risks to this result include recent tariffs on Canadian lumber, which could raise costs substantially and hurt industry confidence.

Housing starts, a measure of new residential construction, will give us another read on this sector on Tuesday. Expectations are downbeat—for a decline to 1.125 million from 1.215 million—but a rise in building permits suggests this report could surprise to the upside.

The Industrial Production report, also released on Tuesday, is expected to show a 0.4-percent gain. Although down from the previous month, it would still be a healthy number. Solid gains in mining and manufacturing are expected to be offset by another decline in utilities output. Results could come in worse than expected, depending on how big that decline is. Manufacturing, which fell unexpectedly by 0.4 percent in March, is expected to reverse course with a 0.4-percent gain, based on an increase in employee hours worked. If the numbers come in as expected, this would be a reasonably healthy report.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg Barclays US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg Barclays US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg Barclays US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million.

###

Mark Gallagher is a financial advisor located at Gallagher Financial Services at 2586 East 7th Ave. Suite #304, North Saint Paul, MN 55109. He offers securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. He can be reached at 651-774-8759 or at mark@markgallagher.com.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2017 Commonwealth Financial Network®