Presented by Mark Gallagher

October lives up to its scary reputation

October provided a roller-coaster ride for financial markets. The Dow Jones Industrial Average ended the month up 2.16 percent, after a drop of more than 5 percent mid-month, while the S&P 500 Index rose 2.44 percent, after a similar drop. The Nasdaq wound up best, posting a 3.06-percent gain, after declining more than 6 percent.

The drop in the middle of the month was caused by a confluence of worries, including the Ebola outbreak, bad economic news from around the world, and weaker-than-expected economic news here in the U.S. Much of the reaction in the financial markets seemed to come from fears that the bad news meant that this was the correction for which everyone had been waiting. In fact, however, with fundamentals continuing strong, most markets rallied after a short-lived pullback and closed October with gains.

Fundamentally, conditions remain healthy. Corporate earnings have been beating expectations—by October’s end, more than three-quarters of reporting companies had surpassed earnings expectations. Revenues have also grown faster than expected, with almost three out of five companies beating revenue expectations. Technically, the trend for U.S. markets remains positive, even with prices having dropped through the 200-day moving average mid-month. The strong recovery since then has brought prices back into a positive trend, and the break itself is not necessarily a danger sign.

Foreign markets showed trends similar to the U.S. market during October, although to different degrees. Developed markets, represented by the MSCI EAFE Index, dropped more than 7 percent mid-month and, despite a late-month recovery, still ended up with a 1.45-percent loss. Emerging markets, represented by the MSCI Emerging Markets Index, did better, with less than a 3-percent loss at mid-month and a 1.07-percent gain by month-end.

The relative underperformance of the developed markets was due to the continued slowing of European growth trends—a result of both the economic impact of sanctions on Russia and growing political conflict between France and Germany. Emerging markets, on the other hand, benefited from a drop in interest rates. Technically, the EAFE remained below its 200-day moving average, which suggested further weakness, while the Emerging Markets index moved back above that trend line, suggesting a resumption of a positive trend.

Fixed income markets also did well following a drop in interest rates, with the benchmark 10-year U.S. Treasury yield declining from 2.489 percent to 2.335 percent during the month. The Barclays Capital Aggregate Bond Index returned 0.98 percent for the month, while high-yield bonds, represented by the Barclays Capital U.S. Corporate High Yield Index, rose 1.19 percent. The drop in rates was due largely to continued declines in European government debt, which drove U.S. rates downward sharply, though they later recovered.

U.S. economic recovery accelerates

Despite the month’s market turbulence, the U.S. economic recovery continued to accelerate. After a disappointing August jobs report, the news that 248,000 jobs had been added in September and that the unemployment rate had dropped to 5.9 percent—close to 2004 levels— showed that the recovery was still intact. Other supporting news included the number of job openings, which reached a 13-year high, and initial jobless claims, which came in at their lowest level since 2000. Improving employment trends led both major consumer confidence measures to seven-year highs.

The Federal Reserve did its part to endorse the recovery by voting to end its bond-buying program and leaving the U.S. economy to stand on its own for the first time in years. Moreover, that move was quickly ratified by the announcement that the U.S. economy had grown at a 3.5-percent rate for the third quarter—above expectations.

Not all of the news was good. Sales of durables were down, which is somewhat worrisome, and consumer income and spending growth slowed. But the majority of the news supported an accelerating recovery. One data point, in particular, was encouraging at month-end. The employment cost index—a sign of pending wage growth—came in at a high for the second quarter in a row, suggesting that the final piece of the recovery, faster wage growth, may be on its way.

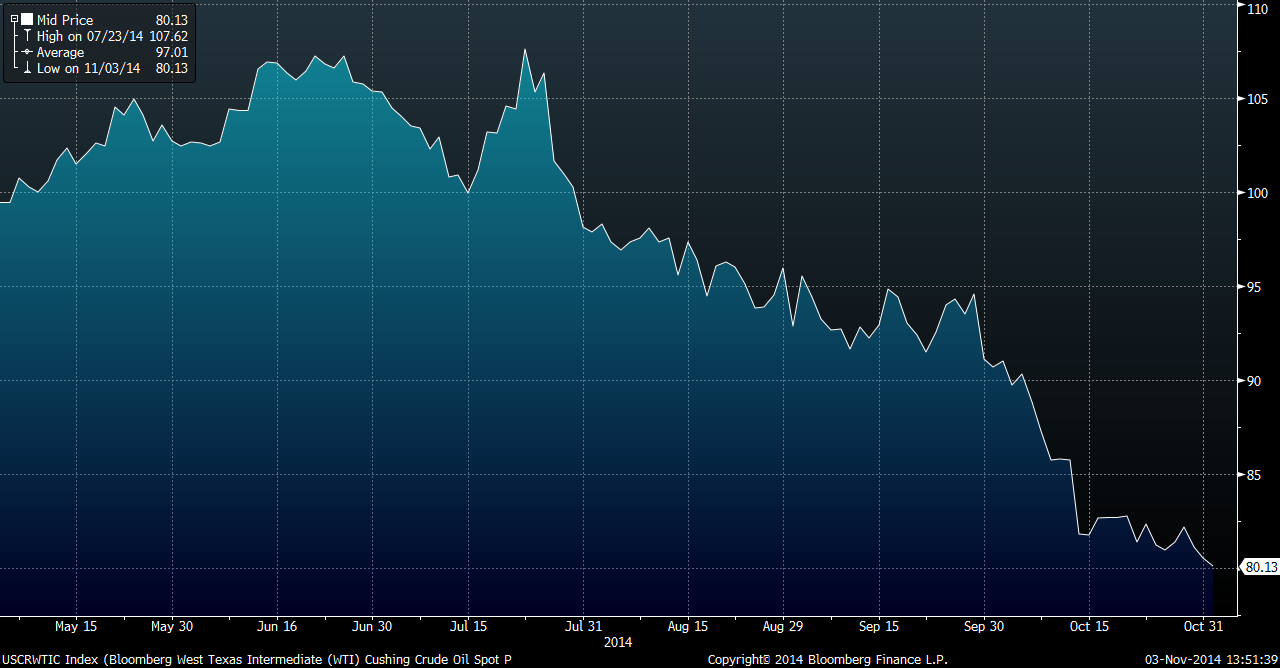

Also supporting growth during the month was a continuing decline in oil prices. As the graph shows, in October oil prices collapsed to levels seen only a couple of times in the past five years.

The Declining Price of Oil, May 15–October 31, 2014

Source: Bloomberg

The drop in oil prices could be a significant boost to U.S. growth. With a $10 change in the price of oil corresponding to roughly a 0.2-percent change in growth, the drop from $95 to $80 a barrel in October could add another 0.3 percent to growth in the next couple of quarters, on top of the already strong figures we now see.

Geopolitical turmoil strengthens the dollar

Continued oil price declines are quite possible, not only from a supply-and-demand perspective, but also as a result of a strengthening dollar. As the price of oil dropped over the past three months, the value of the dollar compared with other currencies increased.

A strong dollar helps hold down the prices of all imports, including oil and commodities, and strengthens the purchasing power of the U.S. consumer. The dollar’s appreciation comes from the growing strength of the U.S. economy, especially compared with the economies of other countries, as well as the Fed’s decision to stop buying bonds, even as Japan continues to do so and the prospect of the European Central Bank starting becomes more likely. With the Bank of Japan’s surprise decision at month-end to increase its bond purchases, and the ongoing economic troubles in Europe, continued dollar strength is likely, which should keep putting downward pressure on oil prices.

The downside of the strong dollar, however, is the probable negative effect on U.S. corporate earnings. Revenue from overseas, when translated to U.S. dollars, will be negatively affected, and this could be a headwind for earnings in the next couple of quarters. Overall, though, the net effect of a strong dollar could continue to benefit the economy and therefore the market.

Halloween much less scary than it might have been

October has historically been volatile, and the extreme price swings of almost all markets during the past month certainly lived up to that reputation. Despite the substantial drop in the middle of the month, though, the improving fundamentals of the U.S. economy and strong position of the U.S. internationally acted to cushion and ultimately reverse the decline.

Markets are inherently risky, and the volatility this month—even though we ended with a gain—should remind us that we will not always be so lucky. Risks remain around the world, and the trends from which we now benefit won’t always be there. It is important to stay focused on the long term and maintain a diversified portfolio that can ride out turbulence in both the short and medium terms.

Economic recovery in the U.S. has laid the foundation for continued profit gains for U.S. businesses, and economic growth has historically led to higher market valuations. This confluence of positive factors suggests that future results should be positive for investors and that the long-term perspective remains the correct one. Although volatility is still possible, and even likely, the longer-term perspective is still bright.

All information according to Bloomberg, unless stated otherwise.

Disclosure: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Barclays Capital Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Barclays Capital government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Barclays Capital U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

###

Mark Gallagher is a financial advisor located at Gallagher Financial Services at 2586 East 7th Avenue, North Saint Paul, MN 55109. He offers securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. He can be reached at 651-774-8759 or at mark@markgallagher.com

Authored by Brad McMillan, vice president, chief investment officer, at Commonwealth Financial Network.

© 2014 Commonwealth Financial Network®