Presented by Mark Gallagher

U.S. markets continue their rise

July broke the streak of strong performance for U.S. equity markets, due in large part to Argentina’s default on its debt and other international turmoil, which knocked markets for a loss at the very end of the month. The S&P 500 Index closed the month down 1.38 percent, the Dow Jones Industrial Average dropped 1.44 percent, and the Nasdaq declined 0.87 percent. Unusually, all three averages had similar performance throughout July, although the Nasdaq was affected least and the Dow most by the international turbulence.

The strong performance of U.S. markets prior to month-end was largely driven by unexpectedly positive earnings news. Per FactSet, as of July 25, more than three-quarters of reporting companies had beaten earnings estimates, while two-thirds had beaten sales forecasts. The overall earnings growth rate was 6.7 percent, but, excluding financials, which was the weakest sector, the growth rate was the highest since the third quarter of 2011. Sixty percent of sectors now have higher growth rates than were estimated as recently as June 30. Sales growth has been strong as well, at 3.1 percent, with 90 percent of sectors reporting an increase. Strong growth in revenue and earnings validates the continuing economic recovery and should provide further fuel for it.

Technical factors were strong for most of July, but the declines in U.S. equity markets at month-end brought all three major indices below their 50-day moving averages, while the Dow also broke below its 100-day moving average. Even though all averages remain well above worrisome levels, these breaks could indicate future market weakness going forward.

Like the U.S., the developed international markets declined in July, with the MSCI EAFE Index down 1.97 percent. The weak results came despite a strong start to the month and can largely be attributed to the growing uncertainty around international events, such as the situation in Ukraine, where a civilian airliner was shot down, leading to worsening tensions with Russia. At month-end, the default by Argentina on its debts, although anticipated, also rattled markets, even as the Ukraine situation drove further sanctions on Russia from the U.S. and Europe. The growing uncertainty apparently further slowed growth, despite the ongoing efforts of the European Central Bank.

On the other hand, emerging markets, as represented by the MSCI Emerging Markets Index, had a very strong month, gaining 1.43 percent for July. After a difficult first quarter, emerging markets have performed well, due to the relative rising risk in developed markets and the faster economic growth of the emerging ones. Technical signs for emerging markets have been positive and improving.

Fixed income also showed losses for the month as rates rose. The 10-year Treasury rate moved from 2.53 percent at the start of July to 2.58 percent at its end. Investors started to move away from the areas of the fixed income market perceived as risky, and this shift, as well as the rise in rates, sent the Barclays Capital Aggregate Bond Index to a loss of 0.25 percent for July.

U.S. economic recovery accelerates out of first quarter

July’s economic reports indicated continued recovery. At the start of the month, employment reports shocked to the upside, with a top-line employment growth figure of 288,000 jobs, continuing a streak of 200,000-plus months. Private employment continued to expand, and government employment also increased materially for the first time in years. This expansion drove the unemployment rate down to 6.1 percent and initial claims for unemployment insurance below 300,000. Gains were widespread, with economists reporting this as the “broadest U.S. employment recovery in 14 years.”

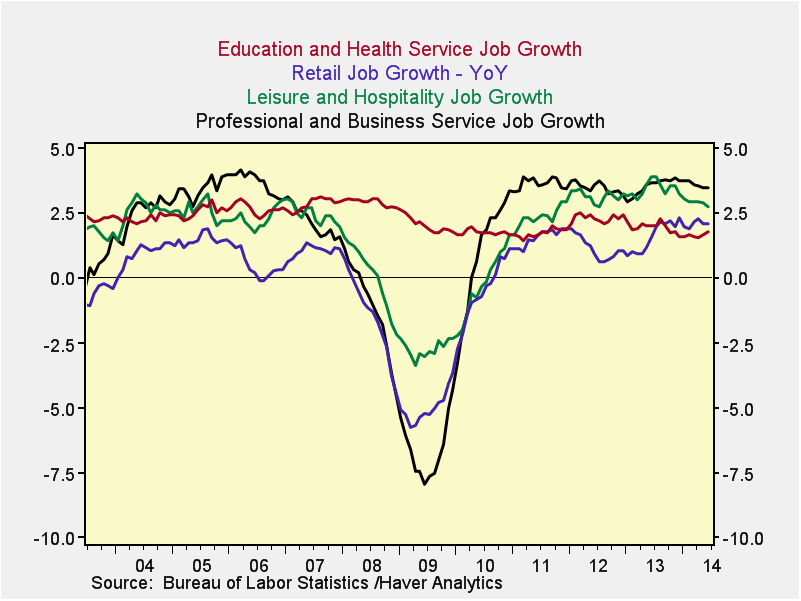

The new jobs were also good jobs. Full-time positions continued to increase, while part-time jobs decreased. The mix of industries and pace of hiring were very similar to 10 years ago, per the chart, which reflects the highest- (e.g., health and business services) and lowest- (e.g., retail and leisure) paying sectors and compares job-growth levels. Not only has job growth normalized, but so has the mix of jobs created.

Other statistics also supported an accelerating recovery. Retail sales growth increased after adjusting for autos and gasoline, as did auto sales. Business surveys conducted by the Federal Reserve showed increasing business confidence across the country, and the trade deficit improved.

Housing showed mixed results, with sales weakening and building permits and starts slowing. Prices, however, continued to increase, and industry confidence increased as well, with the National Association of Home Builders confidence index rising from 49 to 53. Despite the slowdown in sales, permits, and starts, activity and price appreciation approached normalized levels, which will continue to support growth.

Finally, even the Fed endorsed the recovery by stating its intention to end its bond-buying program in October. Although it emphasized that the move would be data-dependent, the fact that it is willing to end its stimulus program suggests that the Fed, too, sees the recovery continuing.

International risks return to the forefront

During July, international risks took center stage. With the Malaysian airliner tragedy in Ukraine, growing conflict with Russia, ongoing Hamas rocket attacks, the Israeli incursion into Gaza, and the ISIS insurgency threatening Iraq’s oil fields, investors were reminded that the world is a dangerous place and that the U.S. is among its safest parts.

Despite the military and geopolitical risks, economic risks also made headlines. The near failure of banks in Portugal and Bulgaria raised fears of the return of the European financial crisis. At the same time, Chinese lending and exports accelerated again—a return to a playbook that China’s government had been trying to change. Finally, the Argentine debt default at the end of the month underscored the point.

As we move into late summer, these risks appear contained. Russia and Ukraine seem stalemated, but no immediate escalation is apparent, even as the U.S. and Europe discuss increased sanctions (which could hurt both the Russian and European economies). Diplomatic efforts continue in an effort to stop the fighting in Gaza, and progress has been made in containing the Iraqi insurgency. Chinese growth is hitting its targets, and the effects of the Argentine default appear limited. In short, although risks have made themselves known, none have broken out. The biggest direct risk remains oil prices, but even there the risks have diminished, with oil prices down on the month.

Good summer weather continues, but storms remain likely

The strong results from the U.S. economy have been encouraging. With both earnings and revenue growing faster than expected, the foundations of the U.S. market have been strengthened. Furthermore, the prospect of future growth provides additional support.

Still, we have been reminded that substantial risks remain. Investors have benefited from a just-right mixture of economic acceleration, economic and monetary policy, and geopolitical calm over the past couple of years. Now, however, because Fed policy has shown signs of changing, conflict has resumed around the world, and economic recovery outside the U.S. has remained weak, there is serious risk that the favorable conditions may well become less so.

Increasing the risk are the current high-valuation and low-volatility levels of U.S. markets. Both factors could lead to significant adjustments if economic and market conditions become less favorable.

In the big picture, though, risk is normal, and the U.S. remains well positioned to ride out any uncertainty, despite potential volatility. As we have seen in the past month, the U.S. economy and financial markets are among the most solid in the world. A well-diversified portfolio with regular rebalancing is still the best way to meet financial goals over time and should be maintained through good times and bad.

All information according to Bloomberg, unless stated otherwise.

Disclosure: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Barclays Capital Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Barclays Capital government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities.

###

Mark Gallagher is a financial advisor located at 2586 East 7th Avenue #304, North Saint Paul, MN 55109. He offers securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. He can be reached at 651-774-8759 or at mark@markgallagher.com.

Authored by Brad McMillan, vice president, chief investment officer, at Commonwealth Financial Network.

© 2014 Commonwealth Financial Network®